GRI 102: General disclosures

GRI 102-18: Governance structure

The governance structure of the organisation (including the committees of the highest governing body) and the committees responsible for decision-making with respect to economic, ecological and social topics are described in the Alpiq Holding Ltd. Annual Report 2020 under the Corporate Governance section.

GRI 102-47: List of material topics

A project team composed of experts from across the Alpiq Group has been set-up in order to define the content of the sustainability report.

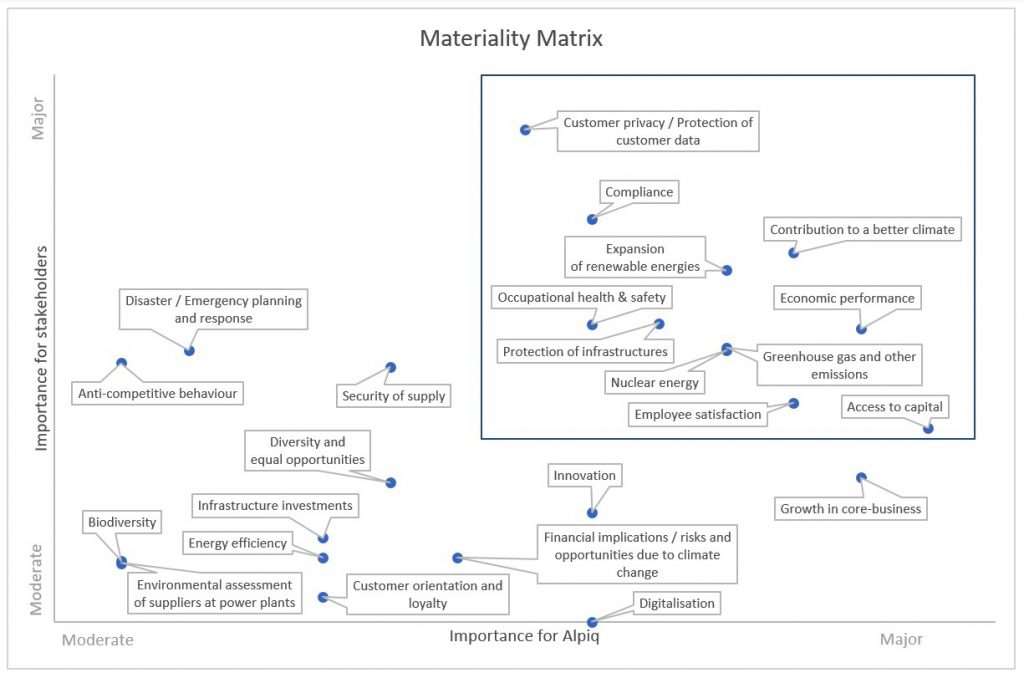

In a first step, the expert team defined the internal and external stakeholders. The most relevant stakeholders have been selected based on an assessment of the influence of the stakeholders on Alpiq and on the significance of the impact of Alpiq’s activities on these stakeholders. A process of stakeholder engagement or dialogue was not performed for this first sustainability report but will be part of the sustainability report 2021.

In a second step, the expert team defined a long list of material topics that must fulfil the following conditions:

- The topics reflect significant economic, environmental and social impacts of Alpiq’s business activity and reflect Alpiq’s purpose and strategy.

- The topics substantially influence the assessments and decisions of the relevant stakeholders.

Finally, those material topics, that were qualified with major importance as well for Alpiq as for its stakeholders, were selected as relevant material topics. The content of the sustainability report is based on these material topics. Both the list of stakeholders and of material topics have been reviewed, completed and approved by a Steering Committee composed of Executive Board Members and Functional Leaders of the Alpiq Group.

The following chart shows the assessment of the material topics based on their significance for Alpiq and on their influence on the assessments and decisions of stakeholders, according to the importance “moderate” and “major”. Important material topics in both dimensions are considered relevant for reporting purposes.